Amentum (AMTM.US): A Misunderstood SpinCo With Huge Potential

A dislocated SpinCo offering investors significant upside through deleveraging and capital allocation

Base Case Estimates & Quick Notes

Amentum is a newly issued diversified government services contractor supplying mission-critical services to the DoD and civilian agencies.

Over the past few weeks, the stock has sold off ~40%, driven by multiple negative headlines and a flurry of selling from a newly established shareholder base.

Deleveraging, merger synergies, and newly unlocked bid capabilities will deliver 10 - 20% EPS CAGR over the next five years.

At 11.5x NTM Adj. P/E and a 10%+ UFCF yield, this stock is far too cheap. We expect significant market outperformance from the stock over the next 3 - 5 years.

Thesis Summary

Jacobs Engineering SpinCo, Amentum (“AMTM”) is a U.S.-based pure-play government services contractor providing mission-critical engineering and human capital to a global military and civilian footprint. The firm's primary exposures are base operations, military training, nuclear waste management, and counterspace services. The entity is an asset-light, human capital-focused services firm that lies somewhere between workforce outsourcing and consulting. Amentum holds contracts with all major government agencies, is the second-largest government services provider by revenue, and is headed by a management team with deep industry expertise.

Despite a seemingly strong setup, AMTM trades at a significant discount to industry peers due to its aggressively leveraged capital structure, exposure to less desirable revenue streams, and lack of financial disclosures. In recent weeks, Trump’s Department of Government Efficiency (DOGE) headlines further depressed the stock, triggering a savage sell-off across the government contracting space.

Amentum now trades at a bargain price on a risk-adjusted basis (9x NTM EBITDA; 11.5x Adj NTM P/E). We think the current setup is exceptionally favorable to investors willing to take a three-to-four-year perspective as we see a clear strategic path to drive strong earnings growth and a meaningful multiple re-rate over the coming years. We believe AMTM can trade up as much as 100% on self-help alone by driving HDD% earnings growth through deleveraging and implementation of PMI synergies.

Better yet, we think mgmt. is at the beginning of a multi-year transformative strategy of divestitures and acquisitions that, with proper execution, will deliver multi-bagger returns.

Recent Events

Trading in Amentum has been choppy, with shares now down ~40% from their November 8th peak and ~30% from the initial spin price in September.

Setpember 24th, AMTM begins trading @ $29.51 after spinning from Jacobs Engineering (NYSE: J)

December 9th, DOGE is unveiled with Trump, Musk, and Vivek loudly touting extreme spending reduction plans. After an 11-day losing streak, Amentum bottoms at a 34% loss.

December 16th, AMTM posts Q1 earnings, sparking a 10% single-day sell-off driven by a weak book-to-bill (0.8x) and worse-than-expected FY25 topline guidance.

Why Does This Opportunity Exist?

DOGE Headlines. DOGE will be a recurring theme in this write-up. Personally, I think the risk is negligible (in fact, I have a pet theory that DOGE will benefit Amentum and the defense services space). Regardless, market jitters around DOGE have driven a hefty sell-off in the space.

Leverage Profile. Amentum’s aggressive 4.0x net-debt-to-EBITDA leverage profile is a big turnoff for historically conservative public investor bases. Note that we believe this is irrational as Amentum’s revenue profile is sticky, contractually profitable, and mission-critical.

Limited Institutional Understanding. Amentum has only been trading for three months, and due to its spin-merger structure, initial financials have been confusing, and a shareholder base has not yet developed.

Business Summary

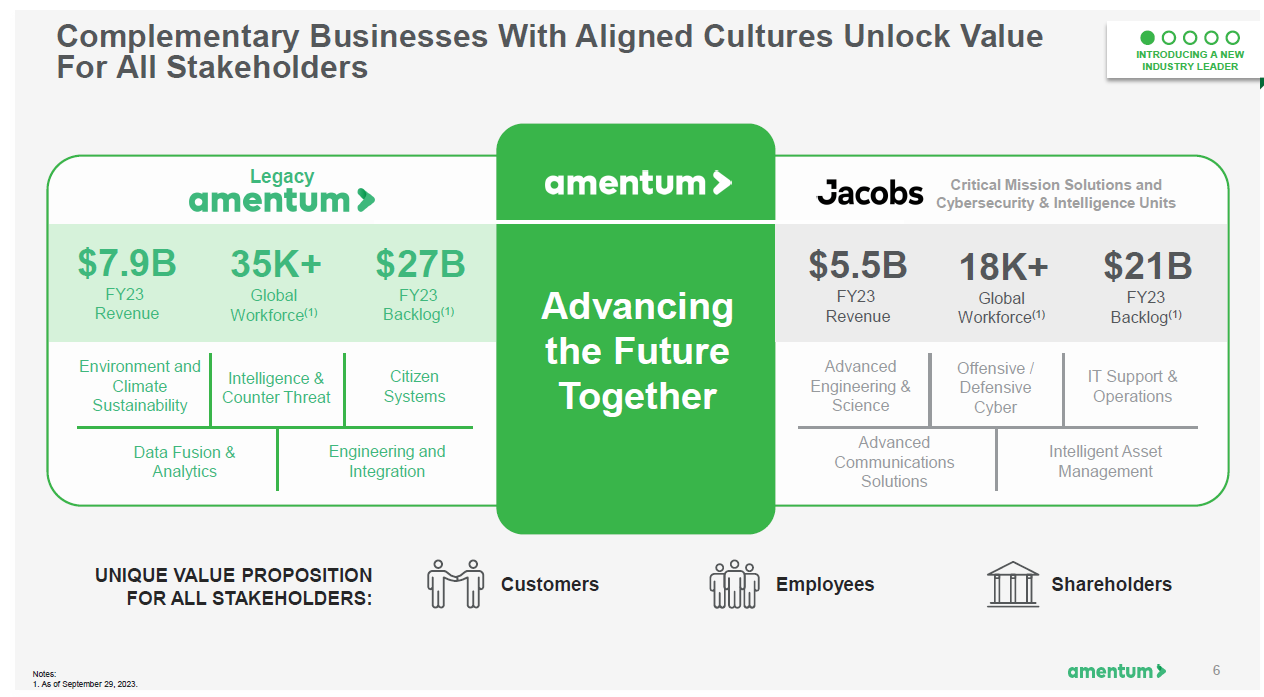

Amentum was created through a spin-merger transaction in September 2024. Jacobs spun its government-oriented cybersecurity & IT services units alongside its nuclear-focused critical infrastructure business into a newly formed entity. This SpinCo immediately went through a merger with PE-sponsored government services roll-up, Legacy Amentum, owned by Lindsay Goldberg and American Securities. The PE sponsors were given a 37% stake in the SpinCo business, with the remainder retained by Jacobs (7.5% of shares) or distributed to Jacobs' shareholders. This new CombineCo adopted the PE platform's name and brought over the Legacy Amentum management team, including CEO John Heller, an industry veteran with a strong track record.

Legacy Amentum was a levered roll-up strategy primarily focusing on "guns-and-guards" contracts (base operations and training) and nuclear waste management / environmental remediation services. The Legacy Amentum platform was built on the 2020 AECOM management services spin, scaled through the acquisition of DynCorp (2020) and PAE (2022) alongside several smaller tuck-ins. While our industry research indicates that Legacy Amentum's nuclear remediation unit is considered a best-in-class operator, the rest of the firm has been seen as sub-par due to historical exposure to a lower margin contract base through low value-added base operations.

Jacobs and Legacy Amentum have well-established operating histories, crucial in the highly bureaucratic and relationship-driven defense contracting world. Amentum holds 90%+ prime contracts and maintains long-term relationships with all major federal agencies, from the DoD to civilian agencies such as FDOT, USCIS, and NASA. Contracts are majority guaranteed margin cost+ or time & materials structure. The New CombineCo is the second largest services contractor by revenue and employs 53,000 people worldwide across 80 countries.

Amentum has a highly diversified contract base and a substantial $45B backlog (~3.2x revenue coverage). Core end market are growing at a 3-5% CAGR with continued growth strongly supported by historic precedent. Further, Amentum’s services are mission-critical for U.S. national security and safety. Key missions include counterspace operations, logistics and base ops. contracts for global strategic assets, nuclear waste remediation, and large-scale training programs for several branches of the U.S. military.

Notably, the new entity’s increased scale and diverse contract base will provide a meaningful advantage as the firm bids and rebids contracts. This will allow for more contract wins, greater contract share, and the ability to go upstream into higher-quality contract types.

Go-Forward Strategy: Unlocking value for shareholders through execution

We see a clear three-to-five-year strategy for Amentum to unlock significant value for shareholders. First, Amentum will direct all or most of FCF to debt paydown as management brings a currently elevated leverage ratio of 4.0x Net Debt/EBITDA to a guided sub-3.0x level in the next 24 months. Deleveraging in this time frame is fully supported by FCFE, but we think there are ample additional opportunities to unlock value and accelerate deleveraging by exploring strategic divestitures of lower margin and more commodified contracts, which will have the dual advantage of shifting rev mix into more desirable (and higher market multiple) areas and directly feeds into part two of our Amentum playbook (see below). We have reason to believe management will explore divestment as (a) newly appointed Executive Chairman Steven Demetriou drove multi-hundred % stock returns over his tenure as CEO of Jacobs by running this exact playbook and (b) we were told directly by management that strategic divestitures of contracts is "very much on the table." Deleveraging should provide some self-help to the story giving FCF yields a nice boost to 12%+ by year-end '26 and opening the door for historically risk-averse gov't services shareholders to get more comfortable with the name.

Part two of the Amentum strategy will come from shifting contract mix. The market currently sees Amentum as lower quality than its direct peers (Leidos, BAH, Parsons, and CACI, to name a few) due to its exposure to base operations and military training programs. These contracts are human capital intensive, LSD% growth, and low margin, with their redeeming qualities being that they are sticky long-term contracts at an effectively guaranteed profit margin and fixed growth rate. For the record, we don't see base ops. contracts as inherently bad but we firmly believe they are better suited in private investors' hands where ample leverage can be applied to deliver strong ROEs. By contrast, public market investors want to see higher margins and more differentiated contract mixes run with very conservative leverage ratios (note that most publics tend to run at 1.5 – 2.0x EBITDA leverage). We think AMTM’s excess leverage profile combined with its less desirable contract base is the primary reason the stock trades at a 30 – 40% discount to peers.

Importantly, management is well aware of this dynamic. We think they will incrementally work to close the valuation gap by capitalizing on IP synergies in the new organization, divesting low-quality contracts to private buyers, and actively focusing on going upstream on contract mix, with a primary focus on IT services, specialized environmental engineering, and defense consulting. These are all areas where the combined entity should have a meaningful foothold in securing new contracts.

We note the direct parallel in Amentum’s market dynamics to Jacobs circa 2016 – 2023 when then-CEO Steven Demetriou executed a series of transformative divestitures and acquisitions, shifting Jacobs from a lowly E&C to the highly regarded IP-driven engineering consultancy behemoth we know today. As a result of strategic shifts under Demetriou's guidance, Jacobs delivered significant profit growth leading to stock price appreciating in excess of 200% during his roughly 5-year tenure. Given that Demetriou retired from his role as Jacobs CEO less than two years ago, we were quite surprised by the announcement that he would take on Executive Chair seat at Amentum. We think the most likely reason for his involvement is a goal of running the same playbook as he did with Jacobs. Moreover, we are convinced that the same playbook of divestitures and acquisitions in the Amentum structure has the ability to unlock meaningful profitability growth and a juicy multiple re-rate for the stock.

In summary, we view Amentum as a rare low-downside; high-upside play. The market may not appreciate Amentum’s current contract base, but we think this is somewhat irrational as revenues are incredibly sticky, show GDP-like growth, and are well insulated from cost-cutting. The stability afforded should ensure that deleveraging can occur without issue. Deleveraging will be a huge tailwind to FCFE over the next few years, with additional kickers in merger-related cost synergies. The cherry on top is that if the firm can pull off a handful of smart divestitures and acquisitions, Amentum may become a best-in-class operator, providing the double benefit of meaningful multiple expansion and margin accretion.

Base Case Valuation

We view Amentum through the lens of a publicly traded LBO. Our base case assumes 100% of available cashflow is used for debt paydown and that organic growth is ~3% p.a. going forward e.g., rev growth tracks historic defense spending. We believe these are conservative assumptions.

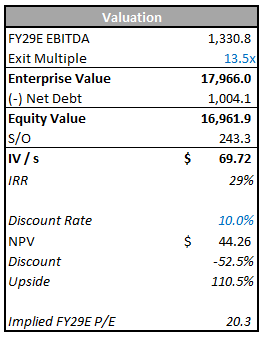

From a multiples standpoint, established contractors (Parsons, BAH, CACI, etc.) essentially trade at homogenous multiples as primes share contracts, sit on majority cost+ business, and grow at similar rates. The group's 10Y average EV/EBITDA is ~13.5x. We will assume this is a fair market multiple and the maximum multiple AMTM can realistically achieve. It’s worth noting that this assumption also may be conservative given the upward trend in multiples since 2013 budget sequestration and that many peers today trade above the 13.5x bogey.

For our base case, we assume Amentum is lower quality and continues to trade at a discount to diversified peers by modeling a 10x EV/EBITDA exit multiple. This should be very conservative, given that a lower leverage profile warrants some multiple re-rate.

These conservative assumptions yield an FY29 price target of $47/s or an 18% 5y IRR. Here is the LBO math demonstrating how the debt-to-equity transfer works:

The Bull Case

In reality, we think management can do better than shown above. As contracts shift upstream, Amentum can likely hit its FY28 EBITDA margin guide of 8.5%—9.0%, scoring a multiple re-rate on the way. Under higher margins and multiple assumptions, we set an FY29 price target of ~$70 / share or a 29% IRR.

A Brief Note on DOGE Risk

The incoming Trump administration has boldly claimed aggressive budget reductions in FY25. DOGE Co-head Elon Musk has gone so far as to state that $2 trillion of $6.8 trillion in government spending will be eliminated during his tenure.

If multi-trillion-dollar budget cuts occur, this would likely be thesis-breaking for Amentum. That said, we cynically believe threatened cuts will not come to pass or will be entirely unimpactful to this industry (a belief well supported by history). There are a number of reasons to think this is the most likely outcome:

(1) DOGE has no real power over federal budgetary spending, as the power of the purse is carried by Congress. In fact, DOGE, or the “Department of Government Efficiency,” isn’t even a real department, as an appointment would also require congressional approval. We don’t see Congress as motivated to enact sweeping spending reforms, at least not in a bipartisan sense. It simply isn’t in the best interest of their re-election.

(2) We think Trump and Musk will quickly clash on ideals, leading to a schism in the current dynamic duo and ultimately jeopardizing the DOGE mission. Further, like all politicians, we note that Trump has a history of overpromising and underdelivering, particularly on government reform. Even if spending cuts come to pass, we suspect they will be much smaller than promised.

(3) Amentum represents a small portion of government spending and provides mission-critical services. We strongly believe that soldiers will continue to require training programs, that government agencies will need more cybersecurity, and that the DOE is unlikely to repeal environmental remediation policies related to nuclear waste management, regardless of the political environment.

All in all, Amentum and the gov’t services space writ large seem well insulated from budget cuts. While it's too early to tell definitively, we think cuts will target largesse in civilian agencies and low ROI R&D budgets given to the Primes (here’s looking at you, Boeing). We note that every subject matter expert and management team we interviewed corroborated this belief.

As an interesting footnote, this is not the first time such a program has been attempted. Here is a fascinating article on REGO, a program initiated 32 years ago by then-Vice President Al Gore.

Summary Financials & Base Case Model

Key Risks

Leverage Profile. At 4.0x leverage, AMTM is less capable than peers to withstand revenue declines and may be impaired when making acquisitions.

Execution Risk. If Amentum fails to delever or improve contract mix by moving into “higher-quality” revenue sources, it is unlikely the stock will re-rate.

Gov’t Spending Reduction. See A Brief Note on DOGE above.

Catalysts

Deleveraging leads to robust earnings growth and a more attractive capital structure for its logical shareholder base.

The market realizes how insulated AMTM is from DOGE.

Under Demetriou’s guidance, management executes strategic divestitures/acquisitions that drive a multiple re-rate.

Conclusion

The Amentum setup today is deeply asymmetric for investors. Amentum is a highly cash-generative, asset-light business with extremely sticky and guaranteed profitable revenue. The market is worried about leverage, government spending cuts, and, more recently, a poor book-to-bill, but does not seem to fully appreciate just how robust this company is.

Once deleveraging gets rolling, FCF yields and EPS will skyrocket, giving management significant flexibility to buy back shares, continue deleveraging, or hunt for tuck-in acquisitions, all independent of market perception.

Amentum can easily double if management does the bare minimum of just deleveraging as promised. With good execution, multibagger returns are on the table over the next few years. Perhaps most importantly, permanent capital impairment seems unlikely even in poor outcomes.

Please leave any feedback, comments, or pushback in the comment section. You can also find me on X @cornerstone127. Write-up suggestions also welcome!

If you enjoyed this and want more of this type of content, please subscribe below. Also, be sure to share with friends, family, and colleagues. Thank you for reading!

Disclaimer: The content on this website is for informational and educational purposes only. Nothing should be considered as investment advice or as a guarantee of profit. Please make sure to do your due diligence. The opinions expressed are those of the author and are subject to change without notice.

Disclaimer: As of the time of writing, the author owns shares in the company described in this article. The author may purchase or dispose of these shares at any time without notice.

Great job, thank you for the effort. I also strongly believe in the company, and have started a position last week.

Thank you for your efforts and post. I agree and find everything you say here on point. Very informative.