YuHua Education (6169.HK): A Chinese For-Profit Educator Trading At 2.0x FCF

Troubled post-reorg offering enormous cash yield and nearing inflection.

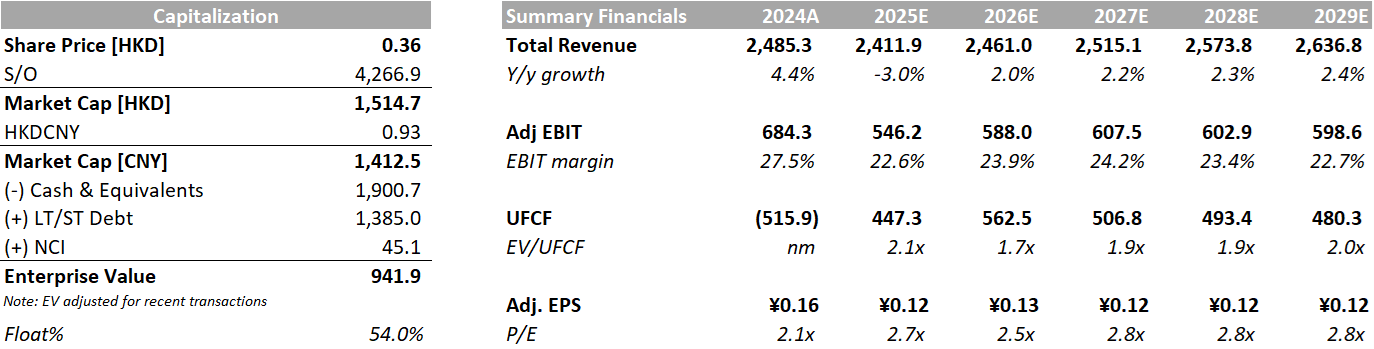

Base Case & Quick Notes

Warning: This idea is highly illiquid and bears significant risk. While I believe and will go on to argue that the risk-reward is favorable, buyers need to be aware that total loss of principal is possible.

YuHua Education (“YuHua”) is a Chinese for-profit high school and higher education operator trading 95% off its 2021 peak.

Declines have been driven by margin collapse, regulatory uncertainty, and, more recently, the restructuring of a convertible note.

Our work indicates that YuHua’s margin compression will moderate going forward, that CCP policy will remain supportive of the space, and that an aggressive capex cycle is at its end, giving way to significant cashflows.

The stock is poised to inflect sharply higher as the market realizes the situation has stabilized. Meanwhile, YuHua is obscenely cheap at 2.0x UFCF and 3.0x P/E.

Thesis Summary

YuHua Education (HK:6169) (“Yuhua”) is a Chinese for-profit educator operating four universities and five secondary schools, primarily in the Hunan province of China. Once a seemingly unstoppable highflyer, YuHua now trades 95% below its 2021 high due to broad regulatory overhang, a surprising and recent default event, and the collapse of its once-high FCF margins.

Despite this frightening backdrop, we believe YuHua stock is poised to inflect sharply higher as its recent capex cycle abates and cost pressures moderate. Further, we believe the recent convertible bond restructuring has derisked the business significantly compared to peers as it eliminated offshore debt and gave a stronger voice to activist shareholders. We expect Yuhua will gush free cash flow in the next twelve months and that this, in combination with the recent bondholder agreement, will allow a reinstatement of the company’s dividend, which will ultimately catalyze the stock higher.

Restructured YuHua trades at 2.8x NTM P/E and 2.2x NTM UFCF, even under conservative assumptions. The company is in a net cash position, and more importantly, all residual debt is held onshore and renminbi-denominated. We believe YuHua will cashflow >100% of its market cap within three years and nearly twice its market cap within five years.

At today’s trading price, barely anything needs to go right for the stock to appreciate. Even if a re-rate fails to materialize, based on a conservative dividend distribution assumption, we expect to receive a solid IRR over the next few years.

Recent Events

July 2021. China rocked investors with a 2021 education policy reform banning for-profit afterschool tutoring and making ownership of compulsory schools (Grades 1 - 9) illegal. YuHua was forced to deconsolidate 19 schools in response.

December 2022. YuHua trading was suspended due to its inability to file annuals, as its auditor was unsure of its ability to repay offshore debt.

January 2023. The company successfully renegotiated bond terms and retired HK$500m in par value of offshore convertible notes. Conversion price on the remaining issue was significantly lowered.

February 2023. Audit financials were released, and trading resumed.

December 2024. Trading suspended again as Yuhua defaults on remaining convertible bond and fails to publish audited year-end financials.

December 2024. YuHua disposes of Thai university (Stamford U) for HK$240m to raise capital for bond repayment.

February 2025. YuHua and bondholders restructure HK$914m convertible into new shares, warrants, and some cash repayment. YuHua shares resume trading on February 27.

Why Does This Opportunity Exist

Investor confidence. The last two years have annihilated investor confidence in the stock. In addition to a default event, margins collapsed, capex spiked without explanation, and IR is unresponsive. If industry sentiment is on the floor, Yuhua sentiment is in the basement.

Regulatory Overhang. In 2021, the CCP blindsided the market by eliminating for-profit tutoring and appropriating private K-9 schools. This sent a message that investors will not soon forget, making the sector untouchable for many funds.

Margin Collapse. YuHua historically earned 60%+ gross margins and spent <10% of sales on capex. Over the past four years, margins have collapsed to <40% while capex has increased 6 - 8x. Investors fear margins will continue to collapse and that capex will never moderate.

Industry Summary

Before digging into Yuhua specifically, let’s first dig into the broader Chinese education industry and its recent woes. The sector is fascinatingly complicated and, ultimately, has been central to China’s emergence from poverty, which has made it a focus of CCP policy. Over the last five years, rapid policy reform campaigns have been implemented to realign the education sector with perceived PRC long-term needs. In a 2021 memorandum, the education system saw a vast overhaul that sent investor sentiment spiraling. Policies included:

Banning of for-profit after-school tutoring that had become ubiquitous and necessary for successful entry into China’s elite university systems.

Banning of for-profit compulsory education (Grades 1 - 9) and a crackdown on foreign investment in compulsory ed.

Requirement that school curricula reflect “Xi Xingping Thought on Socialism with Chinese Characteristics” and a refocus on education as a tool for instilling “Xi thought” in the Chinese youth.

Policy support for vocational education, specifically higher vocational education (e.g., U.S. equivalents of technical colleges).

A focus on fostering for-profit private higher education, specifically within vocational institutions.

The 2021 policy update sent the entire education space into an overnight nosedive. EdTech companies TAL Education (NYSE: TAL) and New Oriental (NYSE: EDU) were rendered effectively worthless, losing 90% of their value following the announcement. Smaller for-profit K-9 educators, such as FHSE, were reduced to VIE shell companies only months after listing in the U.S. Anything remotely exposed to Chinese for-profit education became untouchable due to the risk of appropriation and policy shift.

One corner of the Chinese education market received tailwinds from the 2021 policy: for-profit vocational education. However, this did not stop stock prices from plummeting, as shown in the figure below.

CCP policy support towards vocational education and laxer quota distributions has been a tailwind to the comp group's top-line growth. However, significantly higher reinvestment rates in capex and teaching quality have offset this, leaving EPS roughly flat since the reforms.

Chinese support of the for-profit universities is, at first pass, surprising given their intense crackdown on compulsory and after-school ed. In the broader macro context, however, we believe the CCP is highly incentivized to support for-profit higher ed investment, particularly in the vocational space. China has significant education needs, particularly in rural areas and within specialized vocational services (such as robotics operations or semiconductor fabrication). At the same time, national and provincial budgets are already stretched thin, allowing little room to increase educational capacity.

To continue advancing the middle class, the CCP needs for-profit institutes and private investment to create and maintain the infrastructure required to educate the working class.

This dynamic is clearly displayed when reviewing the details of CCP policy reforms. In the 2021 memorandum, the party explicitly encouraged for-profit higher educational institutions by clarifying that schools could designate themselves as for-profit, allowing greater flexibility in setting tuition and distributing capital.1

Business Summary

Yuhua operates four universities and five secondary institutions (Grades 9 – 12) in China’s Hunan and Shandong provinces. Its primary asset is Zhengzhou Technology and Business University (est. 2002), an independent private general university offering 41 undergraduate majors and 12 vocational programs.

Second to Zhengzhou U is Hunan University of International Economics and Business. Established in 1997, the college was approved in 2000 as a key vocational college in the Hunan province. In 2005, regulators upgraded the college to a fully accredited undergraduate university. Hunan U remains a core resource in the region for applied training (e.g., specialized vocational work) and broader undergraduate programs. We believe Hunan U will be integral to the regional application of Xi's vocational reform policies, as discussed above.

Shandong Yingcai University (est. 1998) is located outside Hunan in the adjacent Shandong province. The college offers 38 undergraduate programs and 37 vocational majors. Provincial administrators have repeatedly selected Shandong U for key educational programs to raise technical ability in the province. They have been recognized as national and provincial leaders in applied engineering.

Zhengzhou Software Vocational and Technical College is the newest entrant to Yuhua’s portfolio, officially opened in Fall 2023. Zhengzhou Tech has the unique distinction of being one of the only official for-profit private higher education institutions in China, as it is one of the few new vocational schools opened since the 2021 for-profit election reform. Zhengzhou was opened in direct response to provincial and party guidance and focuses on new-age technical training (e.g., cloud computing, AI, cybersecurity, and IoT).

Yuhua’s remaining portfolio of high schools primarily operates under single K-12 banners, typically with a Grade 9 - 12 boarding school campus and separate K-9 campuses. Yuhua is actively converting/shuttering these schools due to regulatory risk. Disclosures on the conversion process are poor, but we believe, where possible, dormitories are being repurposed for university use, as evidenced by sustained -15% revenue CAGR in the high school segment despite a stable student population. High schools account for only c.6% of revenue and <5% of gross profit.

Restructuring & Go-Forward Entity

In December 2019, Yuhua issued a HK$2.1bn 0.90% 2024 convertible note to a consortium of offshore investors. The note's conversion price was HK$6.82, a modest markup to the Common’s trading price at issue. Unfortunately for bondholders, Yuhua’s stock plummeted only months after the issuance due to policy changes discussed above. A year after flotation, the note’s strike price was hopelessly out of the money, leaving the debt trading at a considerable discount to par.

In late 2022, bondholders exercised the note’s put provision to cut their losses; however, to everyone’s surprise, Yuhua claimed to be unable to come up with the money to repay the bond. In response, their auditor (PwC Hong Kong) refused to issue audited going-concern financials, resulting in a trading suspension.

This revelation shocked the market as Yuhua had ~HK$4.5bn of cash and equivalents on their most recent balance sheet, far above the HK$2.1bn needed to repay bondholders. Management stated that they could not distribute these funds outside of China and that a significant portion of the cash was earmarked as university operation reserves. As an aside, Chinese firm’s inability to access their capital has become a recurring and disturbing trend leading to bizarre capital allocation decisions, as shown here. Bondholders ultimately accepted a partial repayment of HK$1.1bn in exchange for a restrike on their conversion option.

In December 2024, the remaining convertible par value of HK$930m came due with the restruck call option still far out of the money. Again, Yuhua stated they could not fully repay bondholders. PwC refused to approve the company’s financials, HKEX suspended trading, and Yuhua was cast into a default event, all while having significantly more cash on balance than needed to cover the bond.

Yuhua stock remained suspended for three months while bondholders negotiated a restructuring deal. Ultimately, Yuhua agreed to sell its foreign subsidiary (a Thai-based university) for HK$240m to raise offshore capital. The asset sale was then supplemented with other limited expropriated funds altogether, repaying HK$430m of par value converts. The residual HK$500m par saw forced conversion at HK$0.733 (c.100% higher than the pre-suspension close!). Bondholders also received 182m HK$0.50 strike 3-year warrants.

There are a few critical takeaways from this story. First (and perhaps foremost), Yuhua clearly does not have complete discretion over its bank accounts. China seems to, in principle but not in policy, require universities to collateralize prepaid tuition. Further, there appears to be strict management on how economics are distributed to university owners. We corroborated these beliefs in conversations with Yuhua’s peer Edvantage (HK:0832).

Second, we think Yuhua (and its peer XJ) illuminate a risk not readily apparent to investors. Interest coverage ratios and large cash positions are not inadequate solvency measures in this space. Investors must judiciously review what cash is distributable, what country domiciles the accounts, and to whom / in what currency debt is owed. Yuhua is the only stock in the comp group that is liquid enough to invest in and fits a clean bill of health (e.g., no offshore debt).

Finally, Oasis, a feared East Asian activist fund, underwrote a significant portion of the education boom convertible debt. Oasis already owned 5% of the common, and we expect now owns a substantial portion of the equity. PAG, another highly regarded APAC fund, underwrote XJ debt, and we think also held significant amounts of Yuhua converts. These are not silent partners. Yuhua is the only comparable with an activist shareholder registry and less than 50% family control.

Profit margins stabilizing

Yuhua has seen tremendous margin collapse since its 2021 peak, leading to concerns that the business is fundamentally broken and calling into question where floor margins might be. After 18 months of decline in FCF margins, we believe stabilization is in sight.

Since implementation of 2021 policy, the entire comp group has seen gross margin declines driven by multiple factors. Curricula have needed to be updated or, in some cases, completely rewritten to align with party needs. Campuses have required refreshes for the benefit of students, such as modernizing training labs and expanding campus programs. Student-teacher ratios were required to be brought up (generally targeting 18:1 or better), and scholarship and training opportunities are now required to be supported by the schools.

We don’t view these changes as punitive but rather as a much-needed refresh of the vocational system. Many vocational schools and rural universities have been effectively run as degree mills, with vast underinvestment in student resources and ludicrously poor student training opportunities. Classrooms were often crowded, and teachers were unqualified.

This behavior is no longer acceptable under the new regime. CCP officials will now visit each school and re-accredit the universities. Provincial officials are implementing rules that will require higher education standards, such as minimum post-grad job placement rates and minimum student-teacher ratios.

It’s evident that Yuhua has spent the last decade significantly underinvesting in its campus programs. We estimate that Yuhua entered 2021 with a 30:1 student-teacher ratio and that student training programs were essentially non-existent. Yuhua’s celebrated 67% gross margin was, in hindsight, totally unsustainable. Yuhua’s campuses were also older, and we expect its labs were far out of date. Yuhua had to expedite the turnaround of its campuses in 2022 when it learned that party members would visit the province to recertify the school in 2024.

Through Yuhua's footnote disclosures, we can get a glimpse into the overnight pivot into reinvestment. Teacher headcount increased 50% y/y in February 2023 and moved from 60% of total staff to 80%. Wage expenses alone pressured margins by 8%. We believe university hiring will moderate going forward as Yuhua now has a healthy 16:1 student-teacher ratio.

Another primary cost pressure was scholarship and training awards, which historically accounted for 1.5% of revenue or less. These jumped to 6% in 2022 post-policy reform and have stayed at this level ever since. We don’t see training moderating, but the subaccount has stopped growing now.

Depreciation expense has been the main cost driver of margin compression as Yuhua plowed enormous sums into its fixed assets, raising depreciation as a % of revenue by 300%. Examination of PP&E accounts shows that most additions were marked as “decorations” that depreciate over 5 years. This, in turn, ran capex reinvestment through the PnL at an accelerated rate compared to the past. This corroborates our belief that Yuhua has systematically underinvested in its campuses, requiring dramatic catch-up expenses.

Again, we see moderation here. Party officials visited Yuhua’s schools in mid-2024 and recertified them without issue. With recertification in the rear view mirror, capex fell 99.5% compared to 1H. We expect that Yuhua will be more capital-intensive going forward than it has in the past, but there was a significant fixed asset pull forward to impress party officials and ensure smooth recertification.

Taken together, we think margins have roughly troughed. Inflation in teacher wages might continue to pressure things, but renormalization of capex will flow into depreciation to offset. 2H24 inflected 1000 bps compared to 1H24, which even adjusting for cyclicality, indicates a few hundred basis points of potential run-rate improvement in the pipes.

Valuation

Given the space’s long-term uncertainty, we find traditional multiples-based or terminal value approaches inappropriate. We believe these for-profit ed assets are at high risk of appropriation at some point in the future, and thus, there may be no asset terminal value. Instead, we’ve opted for a three-stage DCF, which allows us to decompose value into three separate and distinct time periods. Our base case assumes that investors receive only five years of cashflows before the business is appropriated.

This model shows our 10-year and 15-year assumption sets:

Valuing only the next five years of cash flow indicates a significant margin of safety on already extremely punitive assumptions. If the business has a TV, the stock is priced at a 60% discount to fair value.

Inputs Notes:

We expect Yuhua’s universities will convert to for-profit in 2027, degrading earnings due to a 15% corporate tax rate requirement.

We use a punitive 15% discount rate due to the high risk of the investment. The company discloses its Goodwill impairment testing uses a 15% rate.

We assume capital intensity remains permanently higher going forward, which we believe is moderately conservative.

Our Base and Bull case imply current fair P/Es of 4.8x and 7.3x, respectively.

Summary Financials

Key Risks

Appropriation risk. The CCP may ban for-profit higher education, rendering the Yuhua stock worthless. We view this as a mid-to-long-term risk and believe the near-term is well insulated.

Inability to distribute cash. The recent off-shore bond default highlights strict capital controls. Despite significant cashflows, offshore investors may never see those profits.

Margin deterioration. The PRC is forcing reinvestment into Yuhua’s schools. Continued reinvestment may further deteriorate margins, possibly until schools are uneconomical. Tuition caps may also be implemented, which would significantly pressure margins over time.

Governance issues. The founding family controls the entity’s common (46% ownership) and owns the licenses through structured contracts. The company’s CEO (37 y/o) is the founder's daughter. Offshore ownership is via a VIE entity, a regulatory grey area. IR is nonexistent; no earnings calls, presentations, or email responses have been provided.

Catalysts

Dividend reinstatement. YuHua suspended its dividend in 2022 due to its convertible bond crunch. With this resolved, we expect a dividend to be reinstated. Even a conservative payout ratio implies a 10%+ yield.

Margin / FCF stabilization. We expect margin declines to moderate as capex drops to maintenance levels and most reinvestment is finished.

For-profit election. YuHua intends to elect for-profit for its schools. It’s unclear what benefits this brings (our model assumes none), but clarifying the for-profit framework should alleviate some investor anxiety.

Conclusion

YuHua clearly bears more risk than the average investment, but we think the option value is significant. At 2.0x UFCF, investors must believe very little about the stock's future to make money. While recent margin collapse and capex are alarming, a detailed review of the expense subaccounts reveals stabilization. We expect Yuhua’s schools will be much healthier going forward, given refreshed campuses, rewritten curricula, and meaningfully improved student-teacher ratios, which will, in turn, improve their brand reputation, possibly driving higher tuitions.

Perhaps counterintuitively, we view the recent convert restructuring as a blessing for prospective shareholders as it eliminated offshore debt, reduced leverage, and put bondholders in control of ~25% of the business. Further, given the binary nature of outcomes, we are excited for warrant trading to begin as we believe the warrant asset may be the best way to play the situation. We expect an optimal position will be a blend of equity and warrant holdings.

YuHua is priced for bankruptcy even though bankruptcy risk has been defrayed. We expect the business to gush cash for the next five years, even under conservative margin and capex assumptions, and we expect a resumption of capital return in short order. YuHua trades at <70% NPV on its next five years’ cash flow or a 60% discount when accounting for a potential TV. Assuming the stock isn’t stolen from shareholders, we expect holders will do well at these prices.

Please leave any feedback, comments, or pushback in the comment section. You can also find me on X @cornerstone127. Write-up suggestions welcome!

If you enjoyed this and want more of this type of content, please subscribe below. Also, be sure to share with friends, family, and colleagues. Thank you for reading!

Disclaimer: The content on this website is for informational and educational purposes only. Nothing should be considered as investment advice or as a guarantee of profit. Please make sure to do your own due diligence. The opinions expressed are those of the author and are subject to change without notice.

Disclaimer: As of the time of writing, the author owns shares in the company described in this article. The author may purchase or dispose of these shares at any time without notice.

Prior policy designated the schools as PNIs, a legal gray area under which profits were extracted, but in theory, the schools were not for-profit.

Thank you for this writeup, I've always wanted to find out more about this whole sector that is trading at such discounted levels.

How were you able to verify the existence and level of offshore debt across peers? Is this documented or did it require IR/management access?

i curious about what is the incentive to convert stock at HK$0.733 (now its hk$0.37) , its mean they gonna make loss when they convert 🤨