Earnings Update: CYND (4256.JP)

The story remains on track.

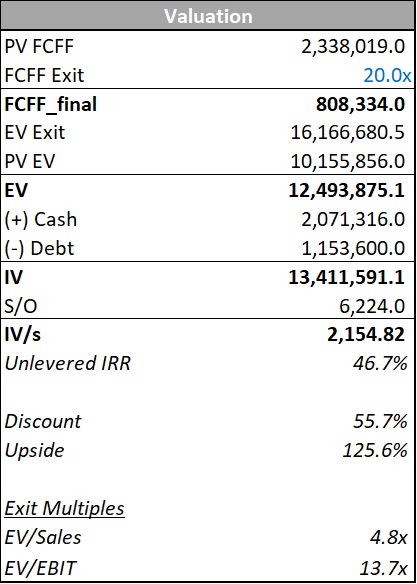

This earnings update should be read in conjunction with my original deep dive:

Quick Take

CYND reported preliminary earnings after the TSX closing bell on April 15th. Preliminary filings in Japan are more of a pamphlet than a full earnings report. Nonetheless, we now know full-year 2025 numbers and core KPIs. Overall, the results were in line with our expectations. The company booked 15% y/y topline growth and guided to 15% growth again next year. Contracted stores increased 18% y/y. New stores were split roughly 50/50 between Kanzashi and BeautyMerit. Gross margins expanded 2.8%, while Adj. EBIT margins were ~flat as the firm increased headcount to continue driving solid growth.

FY26 EBITDA guidance implies a modest (50bps) margin contraction next year, driven by (we think) a ramp in sales efforts. We expected to see margin expansion in FY26, but it seems we underappreciated the level of growth investments could drive. Given that management has guided 300bps+ above our topline expectation, we don’t mind the G&A expansion. Finally, there was a somewhat eyebrow-raising JPY 147m in capex related to standing up their new expanded office space. This expense appears one-time, and we’re willing to brush it off, although communication on the cost could have been stronger.

CYND’s stock opened down 8% on the print after rocketing 20% in the week leading up to the release. Clearly, some shareholders were hoping for more; however, from our perspective, everything performed just fine. At the end of the day, CYND is taking share, growing at double digits, and trading at <10x fwd cashflow. What more do you want?

Let’s unpack the details a bit further below.

Growth Trajectory

ARR, total contracted stores, and revenue all grew ~15% this year. Sales were in line with guidance while EBITDA saw a neat beat of ~5%, driven by significant EBITDA improvement from Pacific Porter (>27% over guide). FY26 guidance shows 15% top-line growth and EBITDA of ~625m, translating to a 25% margin. This is marginally worse than this year’s 25.5% margin, and we think the main difference is increased personnel expense in the sales department.

We initially expected a few percent of margin accretion on a c.12% top-line growth, but we’re more than happy to trade off some margin today for faster market share expansion, so we aren’t disappointed by the change. Ultimately, what matters to us is taking and keeping market share, given the extremely high LTV of customers once CYND is installed.

ARPU was ~flat this year, as was churn, in line with our expectations. If we see a spike in churn or dramatic decline in ARPU, that might be a canary in the coal mine for the idea, so this is a focus for us each print.

Headcount

One of CYND’s primary initiatives has been scaling sales efforts to more proactively match demand. Kanzashi historically had no internal sales team, relying solely on channel partnerships and passive marketing campaigns. CYND’s legacy sales team has also been fairly lean to date, with most sales coming from warm leads generated by channel partnerships or referrals.

We don’t expect dramatic headcount expansions, but we think management will prioritize sales functionality over margin expansion in the near term, given that sales team members drive higher growth. We’re fine with that trade-off, again, so long as G&A expansion really does translate into growth. Below, we’ve laid out employee headcount over time.

New Office

One of the big stories for CYND this year was their move to a larger office space. Employee headcount has expanded by about 50% since the Pacific Porter merger, and the firm simply outgrew its old office. On top of this, management has also indicated that their prior office was a bit homely and that they were ready to get a larger space in a better location to help them attract better talent as they build out their sales team more fully.

Last year, there was a one-time ~81m yen deposit payment. This year, capex totaled ~147m yen, up significantly from last year’s 5.5m yen. There was a one-time ~26m yen moving expense in the third quarter. All in, these are pretty significant charges, albeit mostly one-time.

Honestly, the office move has been poorly communicated from start to finish. I’m sure some language barriers are at play here, but I had to exchange multiple emails with IR to get a handle on costs, the rationale for the move, and the initial deposit. IR didn’t guide on capex during those exchanges, and I was more than a little surprised to see the 147m yen figure.

I don’t think the goal was to obfuscate expenses, but I’m disappointed in the lack of clear guidance and explanation, given the substantial $1.8m capital investment. Hopefully, pictures of the office space and more unpacking of what was bought will come in a future report. Until then, I’ll send some pestering emails to IR.

Wrapping Up

It’s unclear why the stock has dropped so much post-earnings, but, by the same token, it wasn’t clear why CYND’s stock had appreciated so much pre-earnings. One of the big takeaways I’d like readers to have here is that when trading illiquid nanocaps with limited public information, price moves don’t have much signal value. CYND went up 20% on no news. It went down 8% on an earnings print that gave almost no incremental information. I’ve owned this stock for a few quarters now, and can confirm that the number of +/- 5% single-day moves that occur is substantial. Overall, the print aligned with our internal expectations, and we’re excited to keep plodding along, taking market share and accruing semi-permanent cashflow streams with each new contracted store.

Please leave any feedback, comments, or pushback in the comment section. You can also find me on X @cornerstone127. Write-up suggestions welcome!

If you enjoyed this and want more of this type of content, please subscribe below. Also, be sure to share with friends, family, and colleagues. Thank you for reading!

Disclaimer: The content on this website is for informational and educational purposes only. Nothing should be considered as investment advice or as a guarantee of profit. Please make sure to do your own due diligence. The opinions expressed are those of the author and are subject to change without notice.

Disclaimer: As of the time of writing, the author owns shares in the company described in this article. The author may purchase or dispose of these shares at any time without notice.

Good update, helps me understand what KPIs to watch. Any takes on the BM Smart Mirror (bm-smartmirror.jp)? The concept gives me wifi fridge vibes. Plus margin drag from installing and servicing hardware if that's what they're planning to do.

There were other write ups too